Lardaro Report: A Potential Glimmer of Hope

GoLocalProv Business Team

Lardaro Report: A Potential Glimmer of Hope

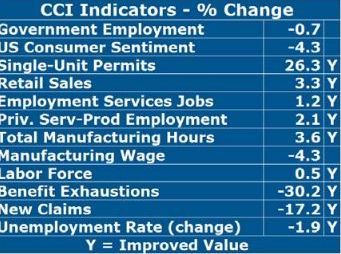

Lardaro stated, "As Rhode Island moves into the third quarter, it appears to have left the disappointing performance from the prior quarter behind - at least for now. The July Current Conditions Index jumped from its neutral value of 50 in June all the way to 75 for July, as nine of the twelve CCI indicators improved. Not only does this improvement come as welcome news for Rhode Island, the increase from June was somewhat expected. I noted last month that the two CCI indicators whose performance put a “nail in the coffin” for June’s CCI, Benefit Exhaustions and New Claims, had displayed bizarre increases that month that were not explainable by any of the obvious undercurrents in our state’s economy. As expected (with my fingers crossed), both went from double-digit rises last month (remember we want both of these to decline) to double-digit declines."

"So, while it is still accurate at this point to say that Rhode Island’s overall performance in 2014 has been disappointing, the July CCI provides us with a potential glimmer of hope that perhaps things here are beginning to strengthen after all as we move through the second half of 2014. Before we get carried away, it must be noted that this July’s CCI reading of 75, while a marked improvement over June, was still below the reading for last July, marking the twelfth consecutive month where the CCI has failed to beat its year-earlier value. I can certainly think of happier one-year anniversaries! So, as Rhode Island moves into the last half of 2014 the most pressing issue continues to be whether Rhode Island’s economic performance will ultimately decouple from the accelerating national economy," Lardaro added.

GET THE LATEST BREAKING NEWS HERE -- SIGN UP FOR GOLOCAL FREE DAILY EBLASTLardaro's Current Conditions Index:

In July, four of the five leading indicators contained within the Current Conditions Index improved, most doing so at healthy rates. Single-Unit Permits, which reflect new home construction, turned in a very strong performance for July, rising by 26.3 percent relative to its value last July. Total Manufacturing Hours, which measures strength in our manufacturing sector, rose sharply again in June (+3.6%), as both the length of the workweek and manufacturing employment displayed significant increases. Oddly, in spite of such strong and sustained manufacturing momentum, the Manufacturing Wage actually declined for a fifth consecutive time in July, by 4.3 percent.

Retail Sales remained strong in July, rising by 3.3 percent compared to a year ago. This indicator has now improved for seven of the last nine months. Private Service-Producing Employment rose by 2.1 percent in July, its strongest rate of growth in over a year. As has been the case for quite some time now, Government Employment fell once again, declining in July by 0.7 percent versus a year ago. Benefit Exhaustions, which reflects longer-term unemployment, reversed its strange double- digit increase of last month, falling by 30.2 percent relative to a year ago. July was the third double-digit improvement for this indicator in the last four months.

Finally, Rhode Island’s Labor Force rose by 0.5 percent versus a year ago in July, the same rate as for June. Along with this, our state’s Unemployment Rate fell to 7.7 percent, moving us to the highly coveted status of #3 nationally. Based on the July CCI, the recent neutral values we observed may well prove to be aberrations. While it is too early to tell for certain at this point, it might be useful to invoke our state’s motto: Hope.

Consistently beating prior-year performance will not only require that we sustain much of the momentum displayed this month, but it will be necessary to see improving Consumer Sentiment, which is likely, along with the resumption of a rising Manufacturing Wage, which may be less likely. Don’t expect to see improving Government Employment any time soon.

RI Business Rankings in US

WalletHub

Rhode Island has 2015's eighth highest insurance premium penalties for high risk drivers, according to a WalletHub report.

Rhode Island ranks fifth overall in the category of speeding over 20 mph annual premium increase at $482. While ranking third overall in the category of 2 accidents annual premium increase at $2,721.

Rhode Island ranks ninth overall under the reckless driving annual premium increase at $749.

WalletHub

Rhode Island has been ranked as the 8th most eco-friendly state in the country, according to a recent study by WalletHub.

Rhode Island ranks third in environmental quality and 16th in Eco-Friendly Behaviors Ran landing them in 8th overall.

RI is behind Washington and New Hampshire who are in the six and seven spots respectively, and in front of Connecticut and Hawaii who come in at the nine and ten spot.

WalletHub

Rhode Island is 2015's 4th Worst State to be a taxpayer, according to a recent WalletHub report.

Rhode Island ranks 48th of 51 with an average state and local tax price of $7,159 which is good for a 27% difference from the national average.

The states that are directly behind Rhode Island are Wisconsin at $7,159, Nebraska at $7,298 and Illinois at $7,719 for a 37% difference from the national average.

WalletHub

Rhode Island has the highest vehicle property taxes in the country, paying an average of $1,133 according to a report from WalletHub.

Virginia and Kansas are the two states just ahead of Rhode Island in the 49 and 50 spots, paying $962 and $905 respectively.

RI also ranks 42nd in average real estate tax, paying an average of $2,779, according to the WalletHub report.

WalletHub

WalletHub has ranked Rhode Island as the 7th worst state to be rich in in a recent in depth analysis of 2015's Best States to be Rich or Poor From a Tax Perspective.

On a scale with 1 being the best, and 25 being average, Rhode Island ranks 37th in low income earners, 42 in middle income earners and 45th in high income earners.

To see the full report, click here.

Gallup

Providence-metro ranks at the bottom for job creation in 2014

Rhode Island has been ranked amongst the worst in job creation, according to a recent survey done by Gallup.

Gallup gives the Prov-metro area an index score of 23, the lowest score is the New York- New Jersey area with 20.

Salt Lake City, Utah and Austin-round Rock, Texas rank the highest with a score of 37.

See the rest of the rankings here.

Forbes

The 2014 state rankings by Forbes has just been released and Rhode Island moved up two spots from #48 in 2013 to #46 in 2014.

What does Forbes say about RI's business environment"

After Michigan and Illinois, Rhode Island has experienced the third worst net migration out of its state in the country over the past five years. With a recent unemployment rate of 7.6%—lower than only Georgia and Mississippi—residents are leaving the state in search of jobs. Rhode Island has been stuck in the bottom five overall for six straight years. One plus: labor costs are 5% below the national average, which stands out in the expensive Northeast.

Tax Foundation

Findings from The State Business Tax Climate Index were released this morning by Tax Foundation which found Rhode Island to have the 45th best tax climate for businesses for 2015. The state's rank has not changed since last year after The Index analyzed 100 different tax variables in multiple categories.

Read more about the report here

WalletHub

After conducting an online suvery consisting of 1,050 individuals from both parties across the nation, WalletHub ranked Rhode Island as having America's 33rd fairest tax system.

Click here to view the poll's entire findings

Thumbtack/Kauffman

Providence is the second worst city in America for small business, according to a new survey conducted by Thumbtack.com and the Kauffman Foundation.

More than 12,000 small businesses in 82 cities across the country participate in the survey. Providence received an overall "F" grade for small business friendliness.

The Economist

Small Business Friendliness Grade: F

The Economist grades states on an A+ to F grading scale for its small business climate. Rhode Island is one of just 6 states to earn an "F" grade.

Overbearing bureaucracy and excessive licensing is stifling small business in America.

Read More About The Economist Grade Here

CNBC

CNBC ranks each state in cost of doing business, economy, technology and innovation.

Rhode Island's unemployment rate as of May 2014 was 8.2 percent. This is RI's lowest unemployment rate since August 2008.

Read More About CNBC Ranking Here

Forbes

Forbes ranks each state in business costs, economic climate, and growth prospects. RI is third worst in 2013.

The most damning in the commentary:

After Michigan, Rhode Island has experienced the second worst net migration in the country over the past five years.

Read More About Forbes Ranking Here

ChiefExecutive.net

#39 ChiefExecutive.net

ChiefExecutive.net ranks each state in taxations and regulations, workforce quality, and living environment.

The most damning in the commentary:

Sky-high unemployment rate bespeaks continuing terrible business climate.

Read More About ChiefExecutive.net Ranking Here

Tax Foundation

#46 Tax Foundation

Tax Foundation ranks each state in corporate tax rank, sales tax rank, and unemployment insurance tax rank.

Rhode Island and the other states in the bottom ten suffer from the same afflictions: complex, non-neutral taxes with comparatively high rates.

Read More About Tax Foundation Ranking Here

Wallet Hub

#24 Wallet Hub

Wallet Hub ranks each state in ROI rank, state tax rank, and overall government services.

Rhode Island ranked #50 for worst roads and bridges, but ranked #4 in safety.

Read More About Wallet Hub Ranking Here

ALEC

#47 ALEC

ALEC ranks each state in economic performance and outlook.

Although Rhode Island ranked low in economic performance, a forward-looking forecast is based on the state’s standing in 15 important state policy variables. Some of these variables include top marginal personal income tax rate and sales tax burden.

Read More About ALEC Ranking Here

Kauffman Foundation

#50 Kauffman Foundation

Kauffman Foundation ranks each state in entrepreneurship.

Entrepreneurial activity generally is highest in Western and Southern states

and lowest in Midwestern and Northeastern states.

Read More About Kauffman Ranking Here

Free Enterprise

#47 Free Enterprise

Free Enterprise ranks each state in performance, exports, innovation + entrepreneurship, business climate, talent pipeline, infrastructure.

Rhode Island has continued to feel the direct impact and ripples from the recent recession—it ranks 47th overall in economic performance. However, positive rankings of 15th in talent pipeline and 16th in innovation and entrepreneurship suggest the existence of a foundation on which to build the future.

Read More About Free Enterprise Ranking Here

The Pew Charitable Trusts

#40 The Pew Charitable Trusts

The Pew Charitable Trusts ranks each state in job growth and job creation.

Rhode Island added 6,223 jobs in 2014.

Read More About The Pew Charitable Trusts Ranking Here

Gallup

10th Worst in Gallup's Annual Ranking of State Job Markets 2014

Rhode Island has been ranked 10th worst for job creation in Gallup's annual ranking of state job markets in 2014 with a job creation index number of 21

Rhode Island is one of two (Connecticut) states to rank in the bottom ten each year since 2008.

The 2014 State level findings have were drawn from 201,254 interviews with employed adults across the nation.

See the full list of rankings here.