Riley: A New Low Cost Strategy for Treasurer Magaziner

Michael G. Riley, GoLocalProv MINDSETTER™

Riley: A New Low Cost Strategy for Treasurer Magaziner

Today’s investment environment is treacherous, especially for those public and private entities who have yet to fund their long term liabilities like Pension Obligations or Insurance, such as long term care or life. Negative or zero interest rates prevail in much of the world making returns of 7 or 8% very difficult for anyone to achieve. This environment has created a new risky asset called long term Government Debt including US Treasuries. In a standard 60/40 asset allocation both stocks and now fixed income expected returns are very low.

A Multi-Strategy Fund

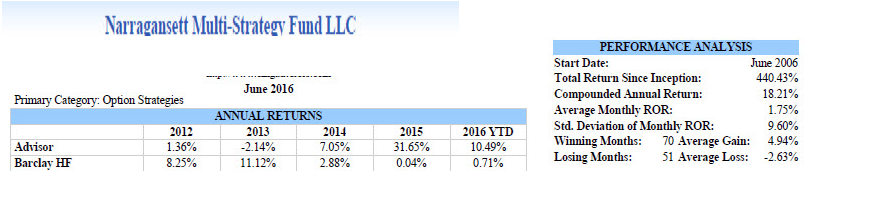

GET THE LATEST BREAKING NEWS HERE -- SIGN UP FOR GOLOCAL FREE DAILY EBLASTAs a financial adviser, fund consultant and professional money manager, I have managed assets 35+ years with great success. Our Hedge Fund, “Narragansett Multi-Strategy Fund," now ten years young, is having its tenth anniversary this month.

Introducing the Buffer or Hedge Strategy

Suppose you could, one year in advance, create a portfolio of diversified stocks virtually matching the S&P 500. Then, let’s say you could design your own parameters of risk and reward to match your outlook. For example, many investors think that today July 2016 market is expensive and returns will be modest, they also believe a 10% correction is more likely than normal. What to do?

We suggest a buffer or hedge strategy that allows for no loss to the investor for the first 10% of the decline after you invest, If the index is down 9% you lose nothing, if the index is down 25% like 2008 you would lose 15%. A more likely scenario would be a market that is up 5% over the next year. Using our hedge strategy your gain is not 5% but is approximately 7% or 1.4x the positive performance of the S&P 500. In order to receive this amazing risk reward, you would have to accept a capped return of approximately 10%.

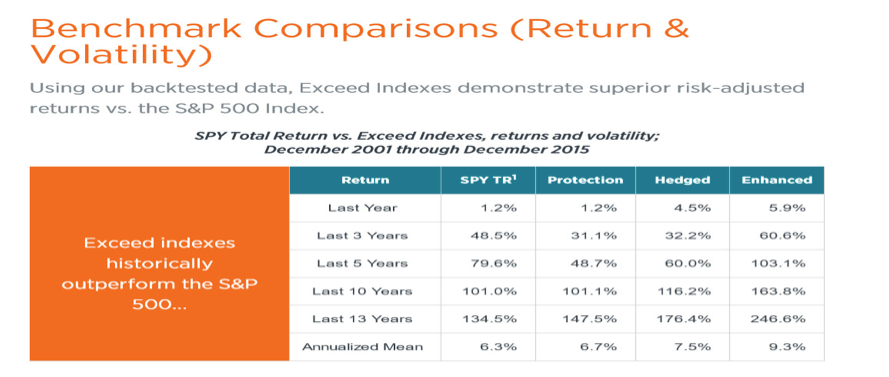

This hedge strategy has been available and used for 20 years or so. Today we are calling for a revolution in pension investing. We think pension funds including Rhode Island would be better off with an 80%-90% allocation to this strategy. Using a combination of one-year term strategies like the hedge above and the “evergreen” strategies developed by Exceed Investments. The evergreen strategies appear above.

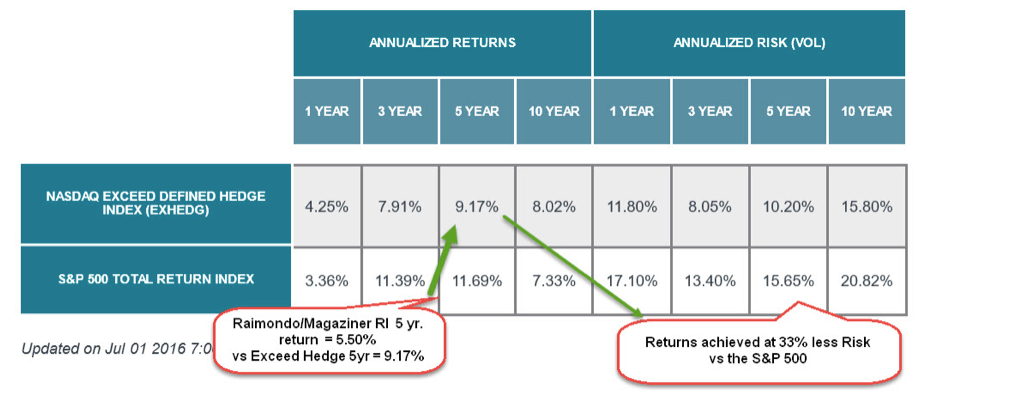

The statistics are amazing and have been confirmed and back tested. The strategies accomplish their State Investment Commission goal of Equity-like returns with much lower volatility and risk. The period above shows the hedge index Outperforming the S&P 500 and at less risk which is shown below. This can be accomplished without 55 different managers, multiple consultants and a large staff. Rhode Island could reduce costs by millions annually. The pension Fund could also reduce fees by 40 million or more.

This is no longer an idea. It is a reality that is made for today’s uncertain environment especially applied to underfunded Pension Plans where owning fixed income assets represent abnormally high risk and low value.

Disclosure: MG Riley is the co-founder of Coastal Management Group LLC, Beach Street Financials Services LLC and CoManages Narragansett Multi-Strategy Fund LLC. Coastal Management Group LLC has an equity stake in Exceed Investments. The advice here is meant for Rhode Island Pension Fund and not a solicitation for investment.

Timeline - Rhode Island Pension Reform

2005-2010

January 2009

Governor Don Carcieri makes pension reform a top priority in his emergency budget plan. His three-point plan included:

1. An established minimum retirment age of 59 for all state and municipal employees.

2. Elimination of cost-of-living increases.

3. Conversion of new hires into a 401(k) style plan.

See WPRI's coverage of Carcieri's proposal here.

2009

Rhode Island increased mandatory employee contributions for new and current employees. New Mexico was the only other state to mandate current employees to increase their contributions.

Read the NCSL report here

(Photo: FutUndBeidl, Flickr)

2010

Rhode Island's state administered public employee pension system only held 48% of the assets to cover future payments to its emplyees.

"This system as designed today is fundamentally unsustainable, and it is in your best interest to fix it" - Gina Raimondo

Check out Wall Street Journal's coverage here.

November 2010

Gina Raimondo defeats opponent Kernan King in the election for General Treasurer of Rhode Island using her platform to reform the structure of Rhode Island's public employee pension system. She received 201,625 votes, more than any other politician on the 2010 Rhode Island ballot.

April 2011

Raimondo leads effort to reduce the state’s assumed rate of return on pension investments from 8.25 to 7.5%.

Her proposal includes plans to suspend the Cost of Living Adjustment (which allows for raises corresponding with rates of inflation for retirees), changing the retirement age to match Social Security ages, and adding a defined contribution plan.

May 2011

Raimondo releases “Truth in Numbers”, a report detailing the pension crisis and offering possible solutions. She continues to work to raise public support for her proposal.

"Decades of ignoring actuarial assumptions led to lower taxpayer & employee contributions being made into the system." - Gina Raimondo (Truth in Numbers)

Read GoLocalProv's analysis of the report here.

Read the Truth in Numbers report here.

October 2011

Governor Lincoln Chafee and General Treasurer Gina Raimondo present their pension reform legislation proposal before a joint session of the General Assembly.

“Our fundamental goal throughout this process has been to provide retirement security through reforms that are fair to the three main interested parties: retirees, current employees and the taxpayer…I join the General Treasurer in urging the General Assembly to take decisive action and adopt these reforms.”- Gov. Lincoln Chafee

October 2011

Head of Rhode Island firefighters’ union accuses Raimondo of “cooking the books” to create a pension problem where one did not exist. Paul Valletta Jr. states that Raimondo raised Rhode Islanders’ assumed mortality rate to increase liability to the state, using data from 1994 instead of updated information from 2008, and lowered the anticipated rate of return on state investments.

“You’re going after the retirees! In this economic time, how could you possibly take a pension away?” Paul Valletta Jr (Head of RI Firefighters' Union)

Read more from the firefighters' battle with Raimondo here.

Check out the New York Times' take on RI's pension crisis here.

November 17, 2011

The Rhode Island Retirement Security Act (RIRSA) is enacted by the General Assembly with bipartisan support in both chambers. RIRSA’s passing is slated to reduce the unfunded liability of RI’s pension system and increase its funding status by $3 billion and 60% respectively, level contributions to the pension system by taxpayers, save municipalities $100 million through lessened contributions to teacher and MERS pension systems, and lower the cost of borrowing.

Read more from GoLocalProv here.

November 18, 2011

Governor Lincoln Chafee signs RIRSA into law. According to a December 2011 Brown University poll, 60% of Rhode Island residents support the reform. Following its enactment, Raimondo holds regional sessions to educate public employees on the effects of the legislation on their retirement benefits.

Read about how Rhode Islanders react to RIRSA here.

January 2012

Raimondo hosts local workshops to explain the pension reforms across Rhode Island. She also receives national attention for her contributions to the state’s pension reforms. The reforms are given praise and many believe Rhode Island will serve as a template for other States’ future pension reforms.

Read about the pension workshop here.

Read Raimondo's feature in Institutional Investor here.

March - April 2012

Raimondo opposes Governor Chafee’s proposal to cut pension-funded deposits. She continued to provide workshops on the pension reforms.

December 5, 2012

Raimondo publicly opposes Governor Chafee’s meetings with union leaders in an effort to avoid judicial rulings on the pension reform package. In response, Chafee issues a statement supporting the negotiations.

Read more about Raimondo's opposition here.

Read about Chafee's statement here.

March 2013

Led by the Rhode Island State Association of Fire Fighters, unions protest the 2011 pension reform outside of the Omni Providence where Governor Lincoln Chafee and General Treasurer Gina Raimondo conduct a national conference of bond investors.

Read about Raimondo's discussion of distressed municipalities here.

April 2013

The pension plan comes under increased scrutiny as a result of the involvement of hedge funds and private equity firms. Reports show that $200 million of the state pension fund was lost in 2012.

"In short, impressive educational credentials and limited knowledge of investment industry realities made Raimondo ideally suited to champion private equity’s public pension money grab." - Ted Seidle (Forbes)

Read GoLocalProv's coverage of the State Pension Fund's losses here.

Read Ted Seidle's criticism of Raimondo in Forbes.

June 2013

Reports show that the State’s retirement system increased in 2013 by $20 million despite the reforms being put into effect the previous year.

Read GoLocalProv's investigation into the rising pension costs here.

September 2013

Matt Taibbi publishes an article in Rolling Stone detailing Raimondo’s use of hedge funds as a questionably ethical tool to aid with pension reform.

Read Taibbi's article in Rolling Stone.

Read GoLocalProv's response to Taibbi here.

October 2013

As Raimondo eyes the role of Governor of Rhode Island in 2014, more behind-the-curtain information about the 2011 pension reform comes to light.

Read more from GoLocalProv about the players in the pension battle here.