Riley: Magaziner Wades Into Rhode Island Municipal Pension Crisis

Michael G. Riley, GoLocalProv MINDSETTER™

Riley: Magaziner Wades Into Rhode Island Municipal Pension Crisis

Not only did the Rhode Island Pension Commission (2012-2015) accomplish very little of its mission, it may have instead encouraged new types of bad behavior. The commission meetings revealed the hopeless dysfunction of several cities and towns and the fact that their elected leaders had purposely avoided funding the pension plan. This in turn gave them money to spend on other more popular projects.

From Bad to Worse

GET THE LATEST BREAKING NEWS HERE -- SIGN UP FOR GOLOCAL FREE DAILY EBLASTAfter studying the final report of the commission and the minutes of 3 years of meetings, I have concluded the commission made things worse. So, I compiled my own statistics of progress from 2011 to June 2016 from multiple sources and Ii is evident that Rhode Island is now far worse off than expected.

At fault were many well-known elected officials serially misleading taxpayers and possibly engaging in criminal behavior in how they did or did not fund pensions. A central criminal question is “Did they mislead municipal bondholders?” Maybe so, but even after all the evidence has been examined, it doesn’t change the facts that we are broke and thus another question remains “Who should pay for this eventual collapse of mismanaged and underfunded local pension plans?”

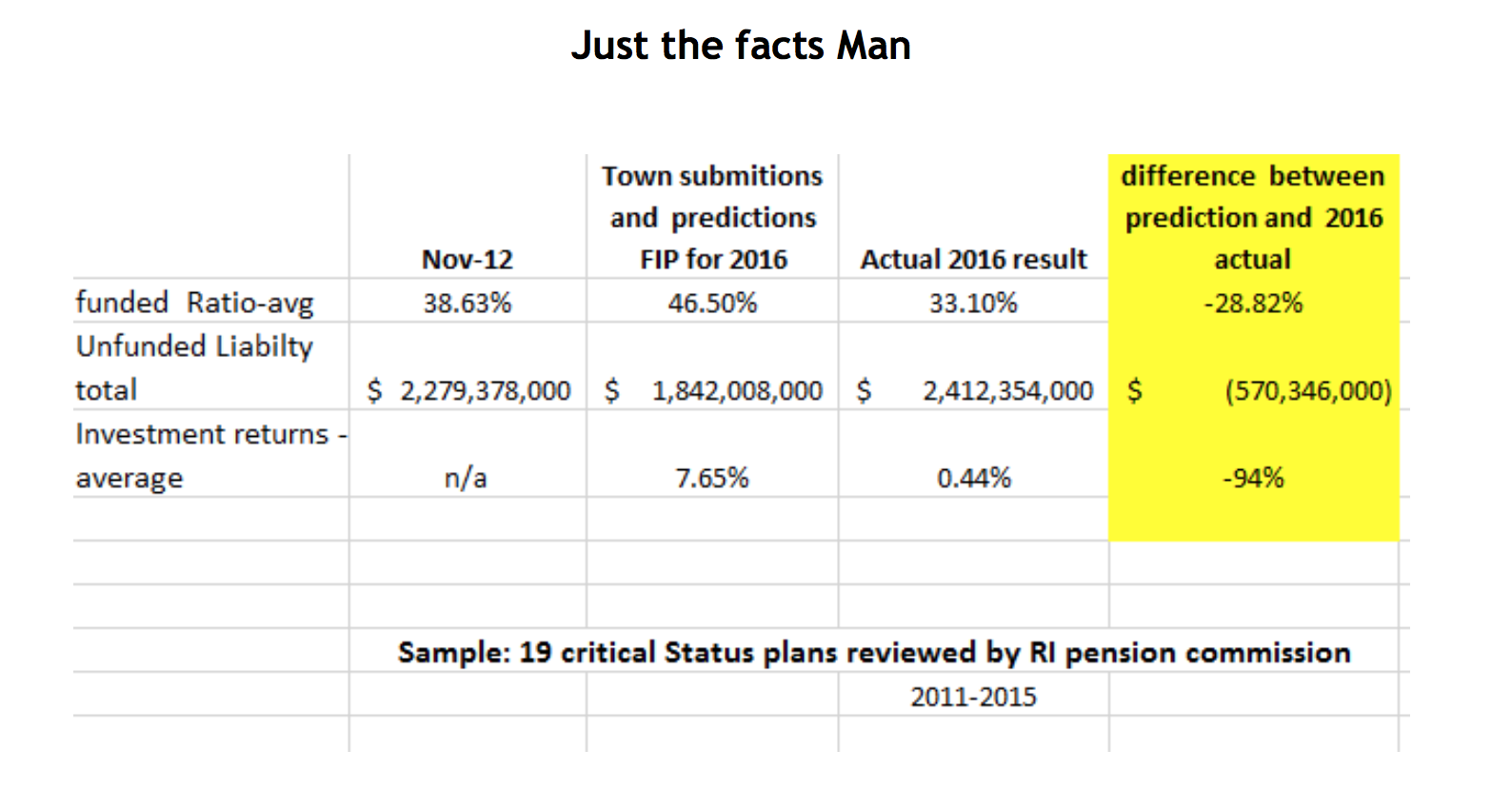

The table above shows the progress, or lack thereof, in Municipal Pension Funding from 2012 to 2016.

It also shows each town 2016 prediction submitted in 2012 as part of their FIP (finding improvement plan). Every crisis town submitted a plan for improving the funding ratio and reducing liability over the next 4 years. As you can see from the table, these RI “critical status” towns failed big time. The funded ratio was expected to improve to 46.5%, but instead the ratio worsened from 38.6% to 33.1%. This means the average town in this study has only 33.1% of the funds necessary to pay for work already done. The national average is 75%.

Unfunded liabilities increased by $ 133 million to $ 2.41 billion, an amazing $570 million more than predicted by the FIP’s. Additionally, the actual 2016 return on investments by the chosen town managers was 94% Worse than predicted at a measly 0.44% vs. 7.65%.

Magaziner to the rescue

Rhode Island State law (2010) places the General Obligation Bondholder in first lien position ahead of the retirees, ahead of the taxpayer and ahead of the public employee.

These teetering towns finances have deteriorated over the last several years. Exacerbated by the hapless toothless commission. I have been yelling from the rooftop to “save the State Taxpayer from bailing out Providence” I am not sure what triggered Treasurer Magaziner’s announcement of a plan to quarantine these “critical status” pension plans and then merge them into MERS (the state run plan). I am sure its political.

However, I agree with the notion that these towns have forever lost their privilege of managing a defined benefit plan. Someone needs to remove this tempting money pot from the control of sneaky and disingenuous finance directors, mayors and councils. Unfortunately, existing state laws, such as the required contribution of 100% or ARC, are completely toothless and everyone knows it. Mayors like Joe Polisena of Johnston openly refuse to fund pensions at all.

“Our approximation is anywhere from five to seven years,” he said of the lifespan until local pension plans are bankrupt.

Polisena, who receives a pension for his 20 years on the fire department, does not believe tax increases are an option either, especially because to cover costs it would well exceed the state cap on how much taxes can be increased in a single year.

“There’s no way there will be a taxpayer bailout to pay for pensions – that’s not the legacy I want to have,” he said. “The system is broken and it can’t be fixed with money.”

Readers know that I’ve been a longtime critic of the pension commission and Ms. Raimondo’s surprising lack of focus on municipal stress.

Although Mr. Magaziner’s’ attempt to address the crisis is welcome, upon reading the details of the proposed legislation I find many of the same problems that plagued the commission. They include lack of accountability, ridiculously low compliance standards and virtually no penalties for negligence or fraud. This makes the proposal a non-starter. A glaring issue is that both Johnston and Providence are belligerent and broke. Then there is the issue of Rhode Island Treasury managing this “critical status” Quarantine plan. Treasurer Magaziner has a lousy money management record and who needs adding this to our State bureaucracy anyway? Next week, a better proposal for the important effort by our Treasurer.

Timeline - Rhode Island Pension Reform

2005-2010

January 2009

Governor Don Carcieri makes pension reform a top priority in his emergency budget plan. His three-point plan included:

1. An established minimum retirment age of 59 for all state and municipal employees.

2. Elimination of cost-of-living increases.

3. Conversion of new hires into a 401(k) style plan.

See WPRI's coverage of Carcieri's proposal here.

2009

Rhode Island increased mandatory employee contributions for new and current employees. New Mexico was the only other state to mandate current employees to increase their contributions.

Read the NCSL report here

(Photo: FutUndBeidl, Flickr)

2010

Rhode Island's state administered public employee pension system only held 48% of the assets to cover future payments to its emplyees.

"This system as designed today is fundamentally unsustainable, and it is in your best interest to fix it" - Gina Raimondo

Check out Wall Street Journal's coverage here.

November 2010

Gina Raimondo defeats opponent Kernan King in the election for General Treasurer of Rhode Island using her platform to reform the structure of Rhode Island's public employee pension system. She received 201,625 votes, more than any other politician on the 2010 Rhode Island ballot.

April 2011

Raimondo leads effort to reduce the state’s assumed rate of return on pension investments from 8.25 to 7.5%.

Her proposal includes plans to suspend the Cost of Living Adjustment (which allows for raises corresponding with rates of inflation for retirees), changing the retirement age to match Social Security ages, and adding a defined contribution plan.

May 2011

Raimondo releases “Truth in Numbers”, a report detailing the pension crisis and offering possible solutions. She continues to work to raise public support for her proposal.

"Decades of ignoring actuarial assumptions led to lower taxpayer & employee contributions being made into the system." - Gina Raimondo (Truth in Numbers)

Read GoLocalProv's analysis of the report here.

Read the Truth in Numbers report here.

October 2011

Governor Lincoln Chafee and General Treasurer Gina Raimondo present their pension reform legislation proposal before a joint session of the General Assembly.

“Our fundamental goal throughout this process has been to provide retirement security through reforms that are fair to the three main interested parties: retirees, current employees and the taxpayer…I join the General Treasurer in urging the General Assembly to take decisive action and adopt these reforms.”- Gov. Lincoln Chafee

October 2011

Head of Rhode Island firefighters’ union accuses Raimondo of “cooking the books” to create a pension problem where one did not exist. Paul Valletta Jr. states that Raimondo raised Rhode Islanders’ assumed mortality rate to increase liability to the state, using data from 1994 instead of updated information from 2008, and lowered the anticipated rate of return on state investments.

“You’re going after the retirees! In this economic time, how could you possibly take a pension away?” Paul Valletta Jr (Head of RI Firefighters' Union)

Read more from the firefighters' battle with Raimondo here.

Check out the New York Times' take on RI's pension crisis here.

November 17, 2011

The Rhode Island Retirement Security Act (RIRSA) is enacted by the General Assembly with bipartisan support in both chambers. RIRSA’s passing is slated to reduce the unfunded liability of RI’s pension system and increase its funding status by $3 billion and 60% respectively, level contributions to the pension system by taxpayers, save municipalities $100 million through lessened contributions to teacher and MERS pension systems, and lower the cost of borrowing.

Read more from GoLocalProv here.

November 18, 2011

Governor Lincoln Chafee signs RIRSA into law. According to a December 2011 Brown University poll, 60% of Rhode Island residents support the reform. Following its enactment, Raimondo holds regional sessions to educate public employees on the effects of the legislation on their retirement benefits.

Read about how Rhode Islanders react to RIRSA here.

January 2012

Raimondo hosts local workshops to explain the pension reforms across Rhode Island. She also receives national attention for her contributions to the state’s pension reforms. The reforms are given praise and many believe Rhode Island will serve as a template for other States’ future pension reforms.

Read about the pension workshop here.

Read Raimondo's feature in Institutional Investor here.

March - April 2012

Raimondo opposes Governor Chafee’s proposal to cut pension-funded deposits. She continued to provide workshops on the pension reforms.

December 5, 2012

Raimondo publicly opposes Governor Chafee’s meetings with union leaders in an effort to avoid judicial rulings on the pension reform package. In response, Chafee issues a statement supporting the negotiations.

Read more about Raimondo's opposition here.

Read about Chafee's statement here.

March 2013

Led by the Rhode Island State Association of Fire Fighters, unions protest the 2011 pension reform outside of the Omni Providence where Governor Lincoln Chafee and General Treasurer Gina Raimondo conduct a national conference of bond investors.

Read about Raimondo's discussion of distressed municipalities here.

April 2013

The pension plan comes under increased scrutiny as a result of the involvement of hedge funds and private equity firms. Reports show that $200 million of the state pension fund was lost in 2012.

"In short, impressive educational credentials and limited knowledge of investment industry realities made Raimondo ideally suited to champion private equity’s public pension money grab." - Ted Seidle (Forbes)

Read GoLocalProv's coverage of the State Pension Fund's losses here.

Read Ted Seidle's criticism of Raimondo in Forbes.

June 2013

Reports show that the State’s retirement system increased in 2013 by $20 million despite the reforms being put into effect the previous year.

Read GoLocalProv's investigation into the rising pension costs here.

September 2013

Matt Taibbi publishes an article in Rolling Stone detailing Raimondo’s use of hedge funds as a questionably ethical tool to aid with pension reform.

Read Taibbi's article in Rolling Stone.

Read GoLocalProv's response to Taibbi here.

October 2013

As Raimondo eyes the role of Governor of Rhode Island in 2014, more behind-the-curtain information about the 2011 pension reform comes to light.

Read more from GoLocalProv about the players in the pension battle here.