Riley: Forecasted 7 Year Returns From Top Analysts Spell Doom for RI Pensions

Michael G. Riley, GoLocalProv MINDSETTER™

Riley: Forecasted 7 Year Returns From Top Analysts Spell Doom for RI Pensions

The CDO (collateralized debt obligation) bubble of 2007 was obvious to many on Wall Street and so was the dot com mania in 2000. We are now living in the greatest bond bubble of all time as Central Bank quantitative easing has created perverse incentives and bizarre pricing of money. All assets are historically overvalued, at least in some magnitude, due to negative interest rates. There are reportedly $10 to $15 trillion perversely invested in negative interest rate bonds. Some optimists have said negative interest rates theoretically produce infinite valuations on steady positive cash flows. Even Warren Buffett has said that, but he also says it could cause chaos.

“That doesn’t mean I think it’s the end of the world when it ends, but I don’t think anybody knows exactly what the full implications of negative rates will be," he said. “I hope to live long enough to find out,” Buffett said.

GET THE LATEST BREAKING NEWS HERE -- SIGN UP FOR GOLOCAL FREE DAILY EBLASTWhich is it? Stocks have infinite value, or they're going to crash?

Negative Interest rate policy is believed to necessary to resist deflationary forces. Central banks are now neck deep in this policy and have no idea how it will unwind. Several analysts warn of huge consequences and a series of rapid-fire adjustments to all asset prices that can be triggered by almost anything. Richard Sylia is one of those analysts and his recent article and video expresses his great concerns.

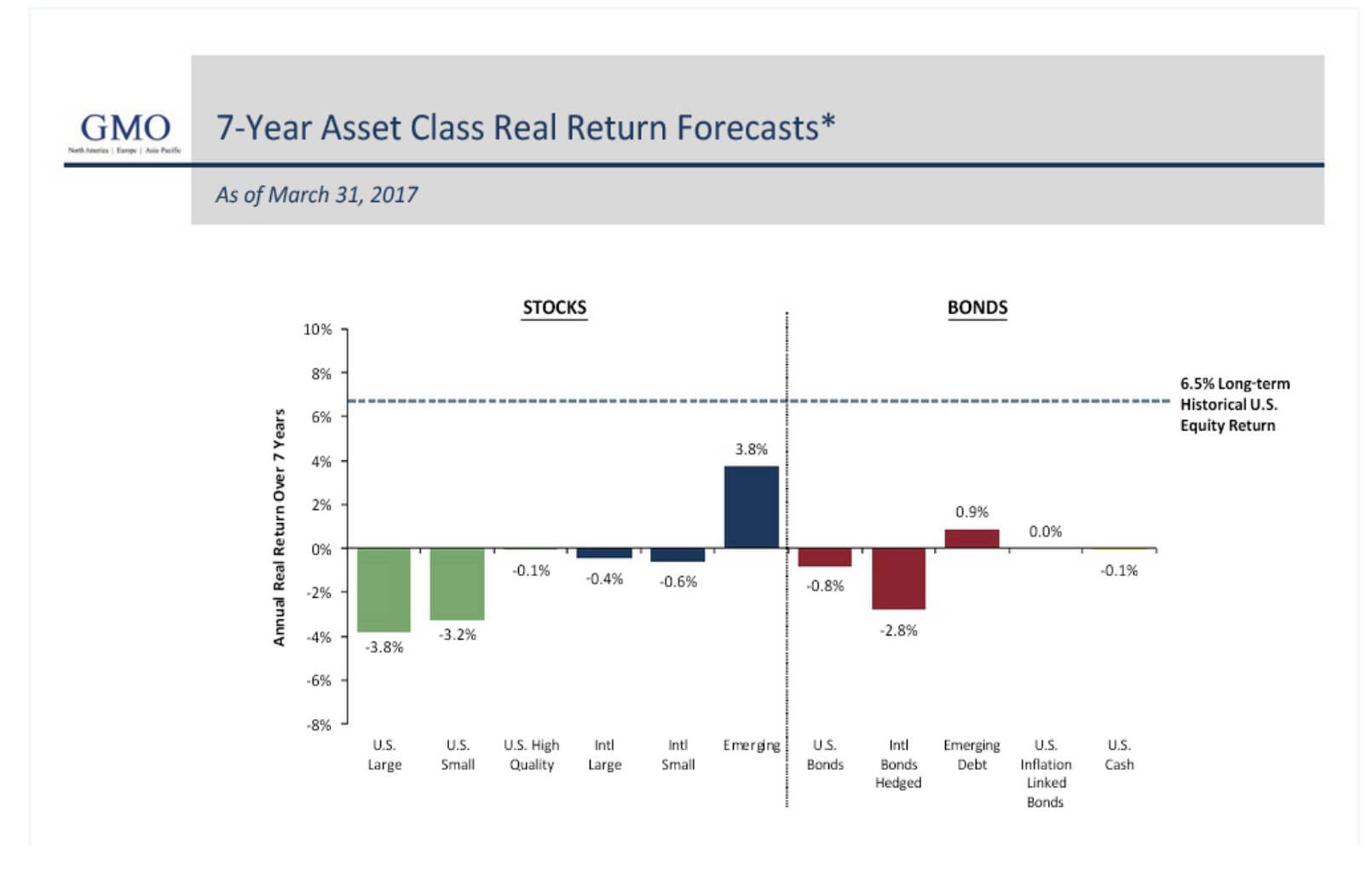

Other analysts such as Jeremy Grantham at GMO and Ray Dalio express concerns about overvaluation combined with unusually low volatility. The world players and stock markets are acting strangely with our economic and political future seemingly balanced on a pin. Daily outbursts from political manic depressives and main stream media have no effect at all on the stock market, which crawls relentlessly higher.

All this strange behavior is a good reason to wait for a dip before investors should be committing new capital. The same advice goes to foundations, investment trusts, and pension fund managers as well. It’s time to take money off the table. Expect a dip of at least 6% before re-evaluating and because the potential for much worse outcomes exist. For readers, it makes sense to have an advisor who understands hedging strategies and can implement them. Let’s Be careful out there!!